Manufacturing cost analysis is essential to achieving reliable cost estimates and securing the best price for purchased parts. This involves breaking down the prices of individual components and comparing them to target costs to identify opportunities for optimization.

Should cost analysis takes a “bottom-up” approach, carefully evaluating all the materials, processes, and service costs involved in production. By adding these elements, organizations can determine the accurate “should cost” of a manufactured product.

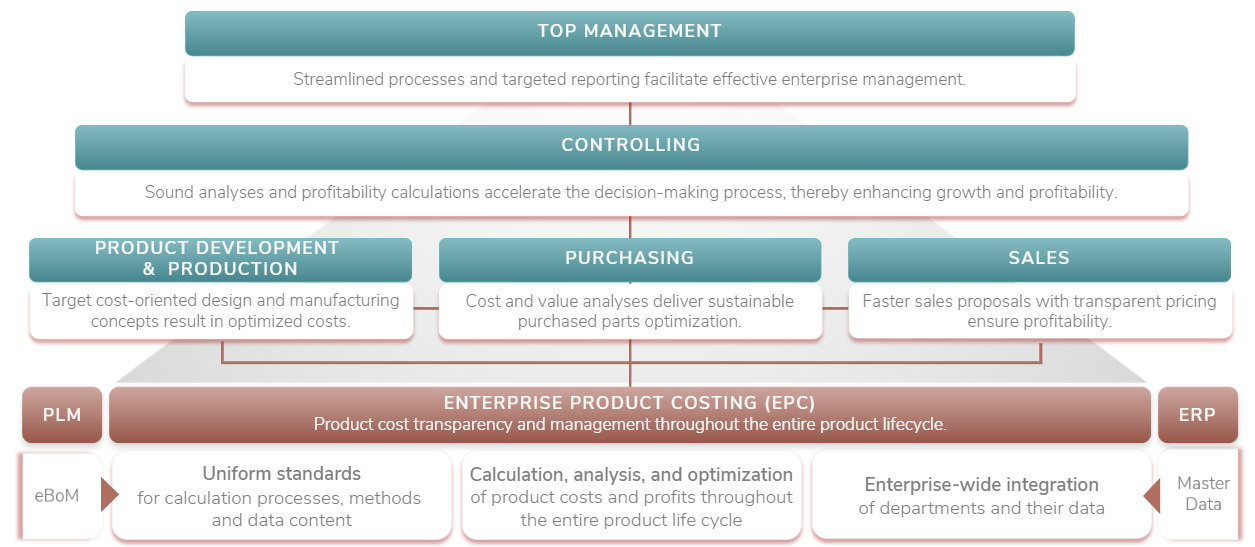

This process requires cross-functional collaboration across teams, including product development, production, cost engineering, and supply chain teams.

Skilled cost engineers are central to this effort. They focus on identifying and prioritizing the most critical cost drivers. By analyzing these components and acting quickly on their findings, organizations can lower costs and speed up the launch of new products.

.png?width=1000&height=508&name=Design%20ohne%20Titel%20(92).png)

Improved Cost Control & Transparency

Clear visibility into costs and real-time data ensures better planning and swift decision-making.

![]()

Strengthened Negotiation Leverage

Data-driven insights help identify overpriced components and secure fair pricing with suppliers.

![]()

Efficient Development &

Procurement Processes

Quick cost estimates and streamlined processes reduce development times and improve efficiency.

![]()

Enhanced Supplier Collaboration

Collaborating with suppliers builds trust, aligns methods, and drives joint cost-reduction efforts.

Should cost modeling is challenging due to its complexity and the required collaboration. Here are the main obstacles that complicate purchasing processes and cost engineering:

A strategic approach, combined with the right should-cost modeling tools, can help address these challenges and pave the way for more efficient purchasing processes.

Should cost models are inherently imprecise due to the complexity of cost drivers.

DO YOU WANT TO LEARN MORE ABOUT OUR FACTON EPC COSTING SOLUTION?

BOOK YOUR DEMO TODAY!